Indiana Medicare Supplement birthday rule: what it means for Hoosiers in 2026

The Indiana Medicare Supplement birthday rule is new as of January 1, 2026 — and most Hoosiers with a Medigap plan don’t know it exists yet. If you’re one of them, this rule could save you real money, every year, for the rest of your life.

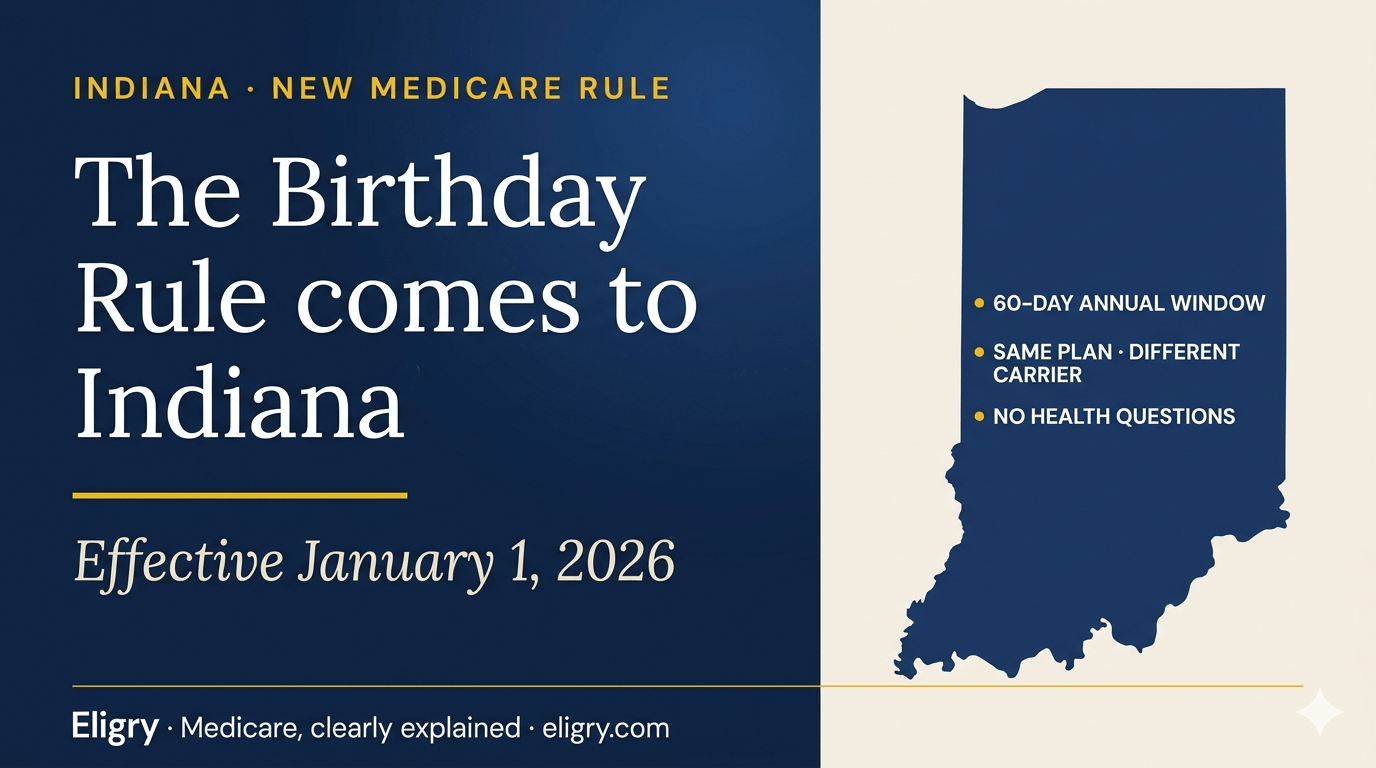

For years, Indiana was one of the many states — like Texas, Georgia, and North Carolina — where switching Medicare Supplement plans meant submitting to medical underwriting — health questions, possible rate-ups, possible denials. That changed with House Bill 1226, which passed in March 2025 and took effect at the start of 2026. The Indiana Medicare Supplement birthday rule now gives people on a Medigap plan a guaranteed 60-day window each year to shop for a better rate, with no health questions and no risk of being turned down.

Here’s exactly how the Indiana Medicare Supplement birthday rule works, who qualifies, and the catches most people miss when they first hear about it.

How does the Indiana Medicare Supplement birthday rule work?

Starting on your birthday each year, you have a 60-day window to switch to the same lettered Medicare Supplement plan with a different insurance carrier — no underwriting, no health questions, no denials. You must be age 65 or older and currently have an active Medigap policy. The law was created by Indiana House Bill 1226 and took effect January 1, 2026.

The key details at a glance:

- Window length: 60 days, starting on your birthday

- Age eligibility: 65 or older

- Plan requirement: you must currently have an active Medigap policy

- Plan switching: same lettered plan only (Plan G stays with Plan G, Plan N stays with Plan N)

- Carrier switching: allowed — you can move to any Indiana-licensed carrier that offers your plan letter

- New coverage effective date: the first of the month following approval

What can’t you do with Indiana’s birthday rule?

You cannot use the Indiana birthday rule to upgrade to a richer plan letter (such as switching from Plan N to Plan G), switch from Medicare Advantage to Medigap, or use it if you’re under 65. It is strictly a same-plan, different-carrier rule — designed to let you shop for a lower premium on identical coverage, not to change the structure of your benefits.

This is where most people get tripped up. The Indiana Medicare Supplement birthday rule is narrower than the birthday rules in some other states, and it’s important to understand what isn’t allowed before you start shopping. I’ve already had clients call me excited about this rule thinking they could use it to upgrade — so let me be clear about the limits.

You cannot upgrade to a richer plan

If you’re currently on Plan N, you cannot use the birthday rule to switch to Plan G, even though Plan G has more comprehensive coverage. The law specifies the same lettered plan type. Want more coverage? That requires medical underwriting just like before.

You cannot switch from Medicare Advantage

The birthday rule only applies to people who already have a Medicare Supplement (Medigap) plan. If you’re on a Medicare Advantage plan and want to switch over to a Medigap plan, the birthday rule doesn’t help you. You’d need to use the Annual Election Period, the Medicare Advantage Open Enrollment Period, or qualify for a separate Guaranteed Issue right such as a trial right or loss of employer coverage.

You cannot use it before turning 65

Indiana residents under 65 who have Medicare due to disability do not qualify for the birthday rule. The law explicitly requires age 65 or older.

People hear “birthday rule” and assume they can use it to switch to any plan they want. In Indiana, that’s not the case. It’s a same-plan, different-carrier rule — designed to let you shop for a lower premium, not to change the structure of your coverage. That’s still a significant benefit, but it’s important to know the limits before you start comparing options.

Why does the Indiana birthday rule matter so much for premiums?

Medicare Supplement premiums typically increase 5% to 15% per year, and before this rule, Indiana residents who developed health conditions after enrolling were effectively locked into their carrier regardless of price. The birthday rule breaks that trap by giving you a guaranteed annual window to shop for a lower rate on the same coverage — with no health questions asked.

If you’ve had a Medicare Supplement plan for a few years, you’ve probably noticed your premium creeping up. That’s not unusual — carriers raise rates on existing policyholders every year, usually somewhere between 5% and 15%. The tricky part is that once you’re locked into a plan, switching to a different carrier used to mean going through medical underwriting, and if you’d developed any health conditions since you first enrolled, you might not qualify for a better rate.

The Indiana Medicare Supplement birthday rule breaks that trap. Every year, regardless of your health, you get a guaranteed 60-day chance to shop the market and see whether another carrier offers the same coverage for less. I’ve already started running these comparisons for my Indiana clients, and the savings are real — for someone paying $180 a month on a Plan G they’ve had for five years, finding another Plan G at $150 saves them $360 per year, and every year after that, until rates catch up.

How does Indiana’s birthday rule compare at a glance?

| Feature | Indiana rule (2026) |

|---|---|

| Effective date | January 1, 2026 |

| Window length | 60 days, starting on your birthday |

| Age eligibility | 65 or older with an active Medigap policy |

| Plan switching | Same lettered plan only (Plan G to Plan G, etc.) |

| Carrier switching | Yes — any Indiana-licensed carrier offering your plan letter |

| Medical underwriting? | No. Guaranteed issue, no health questions. |

| Applies to Medicare Advantage? | No. Medigap plans only. |

| New coverage effective date | First of the month following approval |

How do you actually use Indiana’s birthday rule to save money?

Know your current plan letter, get quotes for that same letter from other carriers during your 60-day window (starting on your birthday), apply with the new carrier, and do not cancel your old policy until the new one is confirmed active. An independent advisor can compare all available carriers at no cost — premiums vary by 20% or more for identical coverage.

If your birthday is coming up and you want to see if you can save, here’s the sensible order of operations:

1. Know which plan letter you currently have

Check your Medigap ID card or your most recent policy paperwork. You’ll need to know whether you’re on Plan A, Plan B, Plan C, Plan D, Plan F, Plan G, Plan K, Plan L, Plan M, or Plan N. Most Indiana residents currently on Medigap are on either Plan G, Plan N, or Plan F (if they enrolled before 2020).

2. Get quotes for that same plan letter from other carriers

This is where an independent advisor saves you time. Different carriers price the same lettered plan very differently in Indiana — the benefits are legally identical (every Plan G covers the same things regardless of carrier, because the federal government standardizes Medigap plan benefits), but premiums can vary by 20% or more between carriers for the exact same coverage. I compare rates across every carrier I’m appointed with in Indiana, so I can show you the full picture in one call.

3. Apply during your 60-day window

The clock starts on your birthday. Some carriers accept applications up to 60 days after the birthday; a few require the signature date to fall within the window but allow the effective date to be later. Either way, don’t wait until the last week.

4. Wait for confirmation before cancelling your old plan

This is the mistake that creates the worst outcomes. Don’t cancel your existing Medigap policy until your new carrier has confirmed your new coverage is active and you have the new ID card in hand. A coverage gap of even a few days at the wrong moment — say, if you have a hospital admission — can cost tens of thousands. I’ve seen this happen to people who assumed the switch would be instant.

Birthday rules are great for consumers in the short term, but they often cause carrier premiums to rise for everyone over time — because carriers lose their ability to price-discriminate based on health. States that adopted birthday rules earlier have seen average annual rate increases climb. Indiana may see a similar pattern. If you find a good rate in 2026, lock it in, but don’t assume the next decade of premiums will stay flat.

How does Indiana’s birthday rule compare to other states?

Indiana’s birthday rule puts it among the minority of states offering annual guaranteed-issue switching. Most states — including Florida, Texas, Georgia, and Virginia — have no birthday rule and require medical underwriting for Medigap switches. New York and Connecticut offer stronger protections with year-round switching. Compared to neighboring Ohio, Michigan, and Illinois, Indiana’s new rule is a significant consumer benefit.

One of the reasons the Indiana Medicare Supplement birthday rule is getting so much attention is that it puts Indiana among the minority of states that offer this protection. Most states — including Florida, Texas, Georgia, and Virginia — have no birthday rule and require medical underwriting for any mid-life Medigap switch. If you split time between Indiana and another state (common for snowbirds heading to Florida), your primary residence matters: the birthday rule applies where you legally reside, not where you happen to be when your birthday rolls around. I live this situation myself — I split time between Highland, Indiana and Sarasota, Florida — so I understand how interstate rules affect real people.

Compared to states with stronger protections — New York and Connecticut allow year-round switching with no restrictions at all — Indiana’s version is relatively narrow. But compared to neighboring states like Ohio, Michigan, and Illinois, Indiana’s new birthday rule is a real and valuable protection. If you live in Indiana and have a Medigap plan, this is something to actively use, not file away and forget about.

For a full comparison of how underwriting rules work across every state where we’re licensed, see our Medicare Supplement Underwriting Rules by State guide.

Want to see if you can save under Indiana’s new rule?

I’m licensed in Indiana and spend several months a year there. Let’s compare your current Medigap premium against what other carriers offer for the same plan — takes about 20 minutes, costs nothing, and you’re under no obligation.

Book a free Medicare plan review Or call (352) 464-4400 — available 7 days a week by appointment