Retirement Planning · Life Insurance · Updated May 2026 · 14 min read

This article is part of the Retirement Mistakes That Can Cost You Thousands series.

Indexed Universal Life insurance is one of the most misunderstood products in all of financial planning.

If you search for information about IUL online, you will find two camps. One side says it is the greatest retirement tool ever created. The other side says it is a scam. Neither is accurate, and both are usually trying to sell you something.

The truth is simpler and more honest than either extreme: IUL is a tool. When designed properly for the right person, it can do things that very few other financial products can do. When designed poorly or sold to the wrong person, it can become a financial burden that takes years to unwind.

I am licensed to sell IUL policies. I also turn people away from them regularly when the product does not fit their situation. This article is my honest attempt to explain what IUL actually is, how it works, who it is designed for, and how to tell the difference between a well-structured policy and one that was built to generate a commission.

I am not anti-IUL and I am not pro-IUL. I am pro-education. People deserve to understand what they are buying before they commit to a financial product that may last decades.

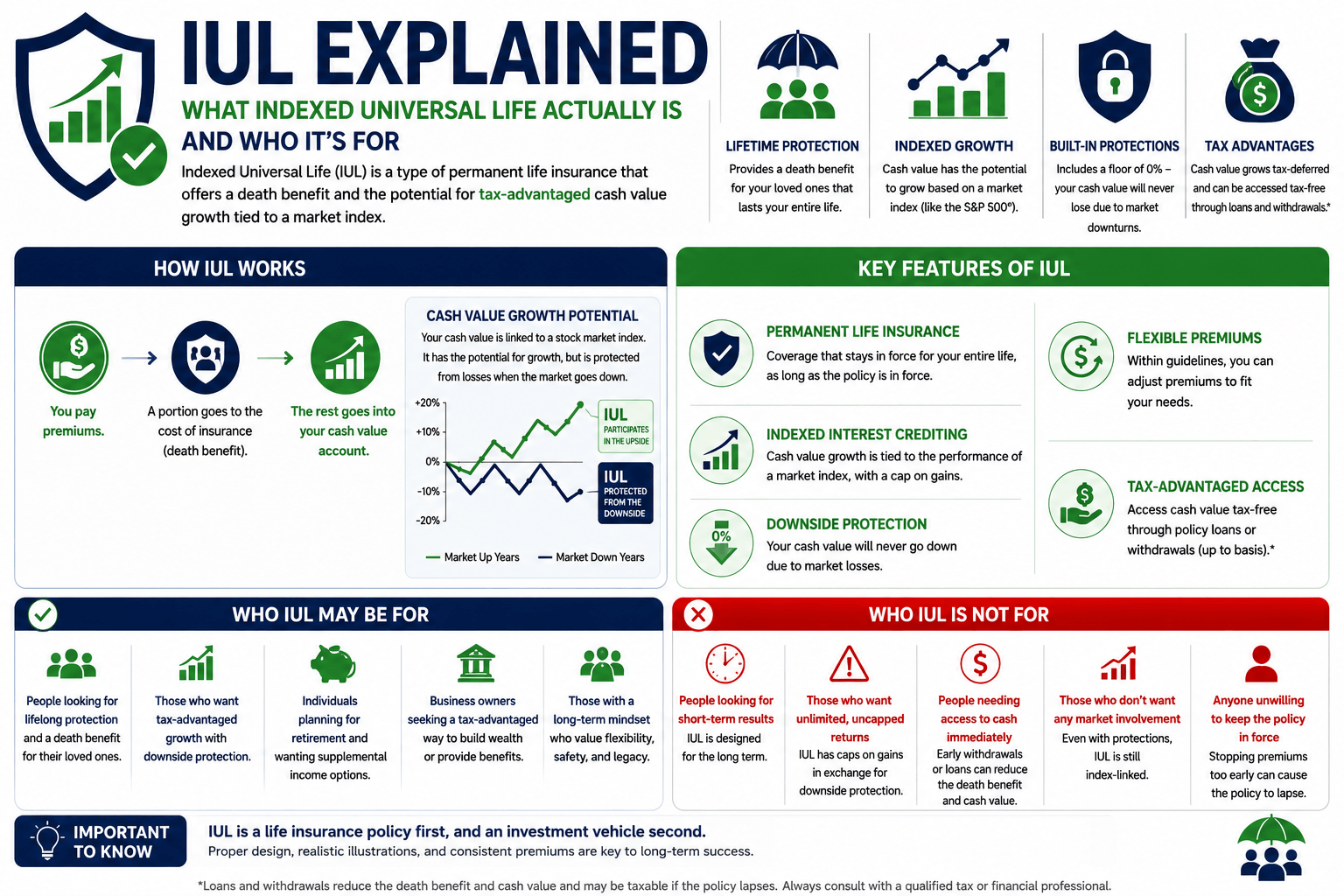

What is Indexed Universal Life insurance?

IUL is a type of permanent life insurance that combines a death benefit with a cash value component whose growth is linked to the performance of a market index — most commonly the S&P 500 — subject to a cap on the upside and a floor on the downside. Your money is not invested in the stock market. The insurance company uses your premiums to purchase options on market indexes, and the returns from those options determine how much interest is credited to your cash value each year.

That distinction matters. You are not buying stocks. You are not in the market. You have no direct investment risk in the traditional sense. What you have is a contract with an insurance company that says: if the index goes up, we will credit your cash value a portion of that gain up to a cap. If the index goes down, your cash value will not lose money from market performance — the floor protects you.

Every IUL policy has two components that work together: a death benefit that pays your beneficiaries when you die, and a cash value account that can grow over time and potentially be accessed during your lifetime through loans and withdrawals.

How do the cap, floor, and participation rate work?

These three numbers determine how much of the market’s gains are credited to your cash value each year. The floor (typically 0%) protects you from market losses. The cap (typically 8-12% in 2026) limits your gains in strong years. The participation rate (typically 50-100%) determines what percentage of the index gain is used in the calculation.

Here is how they work in practice:

| What the S&P 500 does | What your policy is credited (10% cap, 100% participation, 0% floor) | Why |

|---|---|---|

| S&P 500 returns +25% | +10% | Gain is capped at 10%. The carrier keeps the difference above the cap. |

| S&P 500 returns +8% | +8% | Gain is below the cap, so you receive the full amount. |

| S&P 500 returns +3% | +3% | Below the cap. Full credit. |

| S&P 500 returns -20% | 0% | The floor protects you. No loss from market performance. |

| S&P 500 returns -38% | 0% | Even in a crash, the floor holds. “Zero is your hero.” |

The trade-off is straightforward: you give up some upside in exchange for guaranteed downside protection. In a year where the market returns 25%, you only get 10%. But in a year where the market drops 38%, you lose nothing from index performance. Over a 20-30 year period, avoiding the losses can matter as much as capturing the gains — because you never have to dig out of a hole.

One critical detail: cap rates are not guaranteed. The carrier can adjust them, and some do — particularly on older in-force policies. A policy illustrated at a 12% cap today could be running at an 8% cap ten years from now. This is one of the most important factors when evaluating carriers, and it is one of the things most agents gloss over when selling.

What about the cost of insurance charges?

The 0% floor protects you from market losses, but it does not protect you from policy charges. Every month, the insurance company deducts the cost of insurance (COI), administrative fees, and any rider charges from your cash value. In a year where the index returns 0% and the carrier credits 0%, your cash value can still decline because those monthly charges are still being deducted. This is why adequate funding matters so much — and why minimum-premium IUL policies are dangerous over the long term.

Who is IUL actually designed for?

IUL is designed for higher-income earners who have already maxed out their 401(k), IRA, and Roth IRA contributions and want an additional tax-advantaged vehicle for retirement income — while also needing permanent life insurance protection. If you do not need permanent life insurance, or if you have not maximized your other tax-advantaged accounts first, IUL is almost certainly not the right product for you.

The people who benefit most from a properly structured IUL typically share several characteristics:

- They have a genuine need for permanent life insurance (estate planning, legacy, business succession, or income replacement that extends beyond working years)

- They have already maxed out their 401(k), 403(b), IRA, and Roth IRA contributions

- They are in a high tax bracket now and expect to remain in one during retirement

- They have a long time horizon — ideally 15-20+ years before they need to access the cash value

- They can commit to funding the policy adequately every year, not just for the first few years

- They understand this is a life insurance product first and a cash accumulation tool second

Who is IUL not designed for?

If you just need to make sure your spouse can pay off the mortgage if you die, a 20 or 30-year term policy is simpler, cheaper, and a better use of your money. If you have not maxed out your employer match on your 401(k), do that first — it is free money. If you need liquidity in the next 5-10 years, IUL is the wrong vehicle because the cash value needs time to overcome the early-year costs and build meaningfully. And if someone is telling you IUL is a “better 401(k)” or an “investment” — be very cautious about who is giving you that advice and what they are being paid to say it.

What does a properly funded IUL look like vs. a poorly funded one?

The single most important factor in whether an IUL policy succeeds or fails over 20-30 years is how it is funded from the beginning. A properly funded IUL is designed to build cash value efficiently. A poorly funded one is designed to keep the premium low — which is great for the first few years and potentially catastrophic after that.

Properly designed IUL

Funded at or near the maximum non-MEC level from day one. The agent explained the policy costs, the cap rates, the floor, and how policy loans work. The illustration uses a conservative crediting rate — typically 5-6% rather than the maximum allowed. The client understands that this is a life insurance product first and a retirement income tool second. The policy is reviewed annually to ensure it stays on track, and adjustments are made if cap rates change or market performance lags the illustration.

Result: sustainable policy that can deliver on its promises over 20-30 years. Cash value builds reliably. Tax-advantaged retirement income is accessible through policy loans. Death benefit remains intact.

Poorly designed IUL

Minimum-funded to keep the premium as low as possible — often because the client asked for the cheapest option or the agent wanted to make the sale easier. The illustration assumes the maximum crediting rate every year for 30 years — a scenario that has never happened in any historical period. The client does not understand the cost of insurance charges, the loan interest mechanics, or what happens if the market underperforms the illustration. Nobody mentions lapse risk. Nobody schedules annual reviews.

Result: policy underperforms the illustration within 10-15 years. Cash value erodes as COI charges eat into an underfunded account. The client faces a choice: pour more money in, reduce the death benefit, or watch the policy lapse — potentially triggering a taxable event on any gains.

The difference between these two outcomes is not the product. It is the design, the funding, the illustration assumptions, and whether the person who sold it prioritized the client’s long-term outcome or the commission check.

Why are IUL illustrations so misleading?

Because insurance companies are allowed to show hypothetical projections using crediting rates that may never actually occur over the life of the policy. An illustration showing an 8% average return over 30 years looks compelling on paper. But that number assumes the cap rate never changes, the participation rate stays constant, and the index performs at that level consistently — none of which is guaranteed.

The illustration is not a guarantee. It is a projection.

Every IUL illustration includes both a “guaranteed” column and a “non-guaranteed” or “current assumption” column. The guaranteed column shows what happens at the minimum crediting rate (usually 0-2%) — and it almost always shows the policy lapsing or running out of cash value. The non-guaranteed column shows the rosy scenario. Many agents only discuss the non-guaranteed column. That is where the problems start.

When someone shows you an IUL illustration, the questions to ask are:

- What crediting rate is this illustration using? If it is above 6%, ask to see it re-run at 5% and at 4%. If the policy still works at 4-5%, it is well-designed. If it collapses, the design is too aggressive.

- What happens if the cap rate drops? Current S&P 500 cap rates typically range from 8-12%. Ask what happens to the projections if the cap drops to 7% or 6% for an extended period.

- Is this funded at the maximum non-MEC level? If the policy is minimum-funded, the math only works if the market cooperates every single year. That is gambling, not planning.

- What are the total annual costs in years 10, 20, and 30? COI charges increase as you age. A policy that looks efficient at 45 can become very expensive at 70 if the cash value has not grown enough to absorb those rising costs.

- What is the loan rate, and how do policy loans actually work? Tax-free retirement income from IUL comes from borrowing against the cash value, not withdrawing it. If the loan interest exceeds the crediting rate, the policy can spiral.

What are the red flags when someone is selling you an IUL?

After years of reviewing IUL proposals that clients bring to me from other agents, I have seen consistent patterns in how poorly designed policies are sold. These are the warning signs:

- The agent calls IUL an “investment” or a “better 401(k).” IUL is a life insurance product. It has insurance characteristics, insurance costs, and insurance regulations. Calling it an investment is misleading and, in some states, a compliance violation.

- The illustration uses a crediting rate above 7%. Historically achievable? Maybe. A responsible basis for a 30-year projection? No. Ask for 5%.

- The agent never mentions the guaranteed column. If someone only shows you the sunny-day scenario, they are not educating you. They are selling you.

- The policy is minimum-funded. A low premium sounds attractive but it means the cash value has no margin for error. One bad decade and the policy is in trouble.

- No annual review is discussed. An IUL policy is not a set-it-and-forget-it product. Cap rates change, markets fluctuate, and COI charges increase with age. Without annual reviews, small problems become big ones.

- The agent cannot clearly explain how policy loans work. If they cannot explain the loan mechanics — fixed vs. variable loan rates, wash loans, spread, and the impact on death benefit — they do not understand the product well enough to be selling it.

- You are told you do not need other retirement accounts. If someone suggests IUL instead of maxing your 401(k) match, they are putting their commission ahead of your financial well-being.

What can a properly structured IUL actually do?

When I say IUL can be a valuable tool for the right person, I mean specifically these things:

Permanent life insurance protection. Unlike term insurance that expires after 20 or 30 years, IUL provides a death benefit for your entire life as long as the policy stays in force. For estate planning, business succession, or income replacement that needs to last beyond working years, permanent coverage is sometimes the right answer.

Tax-advantaged cash value growth. The cash value grows tax-deferred. You do not pay capital gains tax on the annual crediting. Over 20-30 years, this tax-deferred compounding can be significant — especially compared to a taxable brokerage account.

Tax-free retirement income through policy loans. When structured properly and funded adequately, you can borrow against the cash value in retirement. Policy loans are not taxable income as long as the policy remains in force. For someone in a high tax bracket, this can be a meaningful complement to other retirement income sources.

Downside protection. The 0% floor means your cash value is not exposed to market crashes. In a year like 2008 when the S&P 500 dropped 38%, an IUL policy holder received 0% — they did not participate in the recovery, but they also did not have to dig out of a 38% hole. Over long periods, avoiding catastrophic losses can matter as much as capturing big gains.

Flexibility. Premiums are flexible within policy limits. Death benefits can be adjusted. Allocation between indexed and fixed accounts can be changed. For someone whose income or needs may change over time, this flexibility has value.

How I approach IUL with my clients

When someone asks me about IUL, the first thing I do is ask whether they actually need it. If they have not maxed their 401(k) match, I tell them to do that first. If they do not need permanent life insurance, I tell them IUL is probably not the right product. If they need coverage for 20-30 years and nothing more, I show them term insurance.

If IUL does fit their situation, I design policies conservatively. I illustrate at 5-5.5% rather than the maximum. I fund at or near the maximum non-MEC level. I explain the guaranteed column and what it means. I explain how policy loans work, including the risks. I schedule annual reviews, and I adjust the policy if cap rates change or performance lags.

I also tell clients to get a second opinion. If someone has already been shown an IUL illustration by another agent, I will review it and tell them what I see — whether the design is sound, whether the assumptions are realistic, and whether the funding is adequate. There is no charge for that review, and if the other agent’s proposal is better than what I would build, I will say so.

My goal is not to sell you an IUL policy. My goal is to make sure you understand what you are buying — or what you were sold — so you can make a decision you will not regret in 20 years.

Frequently Asked Questions

Is IUL a good investment?

IUL is not an investment — it is a life insurance product with a cash accumulation feature. It can support a retirement income strategy when properly structured and adequately funded, but it should not be compared to stocks, mutual funds, or index funds. It serves a different purpose and has different characteristics.

Is IUL better than a Roth IRA?

For most people, a Roth IRA should be funded first because it has lower fees, more flexibility, and no insurance costs. IUL becomes relevant after you have maxed out your Roth IRA and other tax-advantaged accounts and still want additional tax-free retirement income combined with permanent life insurance. They are not competitors — they serve different roles. Full comparison: IUL vs Roth IRA →

What happens if my IUL policy lapses?

If the cash value drops to zero and you cannot or do not pay enough premium to keep it in force, the policy lapses. You lose the death benefit. And if you had taken policy loans against the cash value, the outstanding loan balance may become taxable income in the year of the lapse. This is the worst-case scenario and the primary risk of an underfunded IUL.

Can the insurance company change the cap rate?

Yes. Cap rates are not guaranteed. The carrier can adjust them based on market conditions and the cost of the options they use to hedge your index credits. This is why it is important to choose a carrier with a strong track record of maintaining competitive cap rates on in-force policies, and why annual policy reviews matter.

How much should I fund an IUL?

Ideally at or near the maximum non-MEC (Modified Endowment Contract) level. Funding at this level maximizes cash value growth while preserving the tax-advantaged treatment of policy loans. Minimum-funding an IUL is one of the most common mistakes because it leaves no margin for error if markets underperform or cap rates decrease.

Does it cost anything to have Cindy review my existing IUL policy?

No. If you have an existing IUL policy and want a second opinion on whether it is properly structured and adequately funded, I will review it at no cost. If the policy is sound, I will tell you. If it needs adjustments, I will explain what to ask your current agent or carrier.

Talk to Cindy — It’s Free

Whether you are considering an IUL for the first time or want a second opinion on a policy you already own, I am here to give you honest, independent guidance. No pressure. No obligation.

Schedule My Free Consultation ☎ (352) 464-4400Available 7 days a week · I’ll tell you honestly if IUL is not the right product for you.

Related Reading

Cindy Kowalski is the founder of Eligry LLC, a licensed independent Medicare and retirement advisory firm serving clients in 22 states. She holds AHIP 2026 certification, is licensed in life insurance and retirement products, and has more than 40 years of business experience including 23 years in enterprise sales at AT&T and 16 years running an IT consulting firm. She is not employed by or exclusively contracted with any insurance carrier. NPN 21601670.

This article is for educational purposes only and does not constitute financial, investment, tax, or legal advice. Indexed Universal Life insurance involves risks including potential loss of premium, policy lapse, and tax consequences. Policy guarantees are subject to the claims-paying ability of the issuing insurance company. Consult a qualified professional before making any financial decisions. Not affiliated with or endorsed by the U.S. government or the federal Medicare program. © 2026 Eligry LLC.