Most people think of Social Security as a simple decision: you hit a certain age, you file, you get a check. But the age you choose to claim is one of the most consequential financial decisions you’ll make in retirement — and unlike most decisions, this one is essentially permanent.

Claim too early and you lock in a reduced benefit for life. Wait too long and you may have spent years drawing down savings you didn’t need to touch. The “right” age depends entirely on your health, your income sources, your spouse’s situation, and — this is the part almost nobody talks about — how your Social Security income interacts with your tax bracket and your Medicare premiums.

This page walks through the real math, the real trade-offs, and the questions you should be asking before you file.

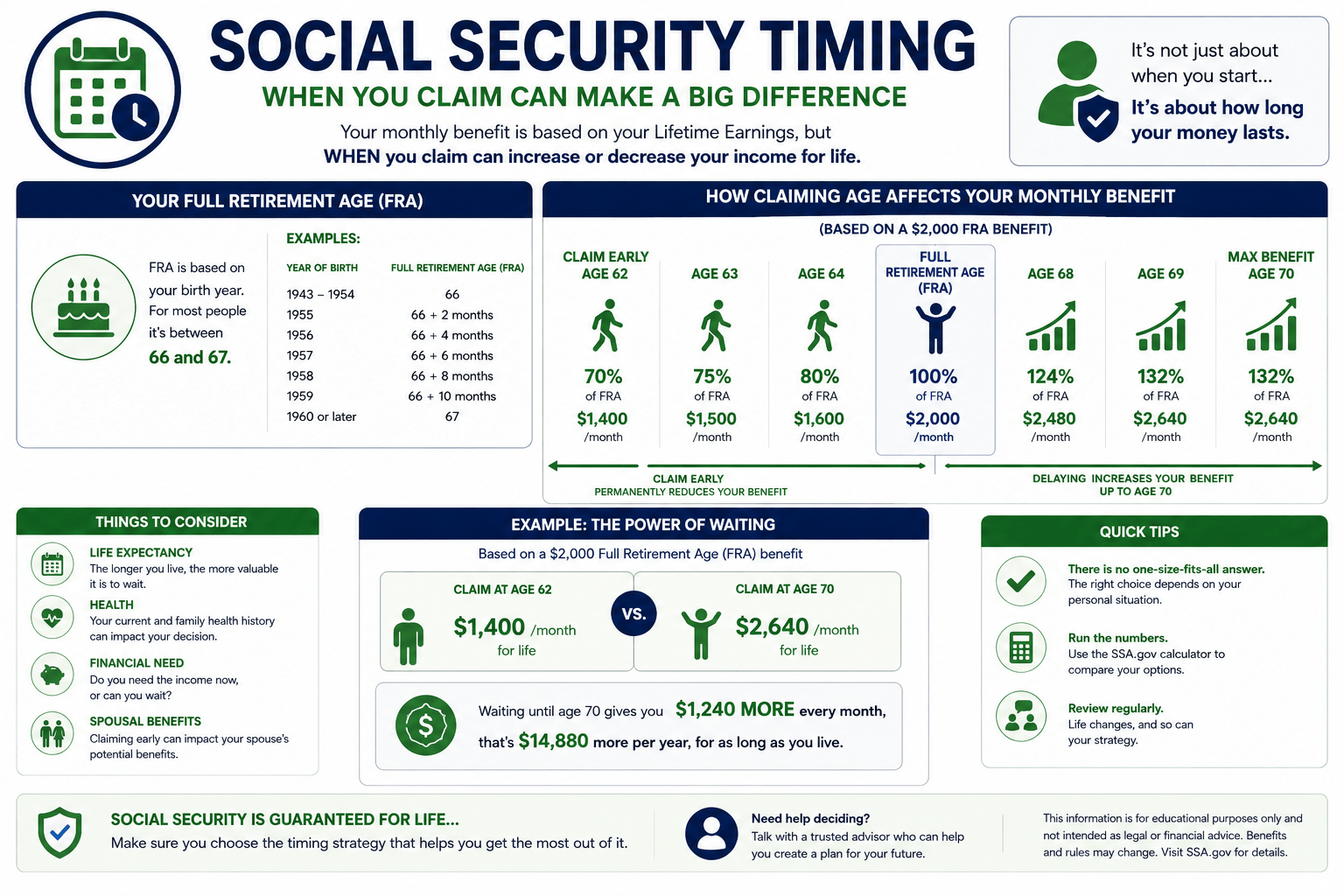

The Three Ages That Matter: 62, 67, and 70

For most people born in 1960 or later, your full retirement age (FRA) is 67. That’s the age where you receive 100% of the benefit you’ve earned over your working career. The two other ages that matter most are 62 — the earliest you can file — and 70, the latest age where delaying still increases your benefit.

| Claiming Age | Effect on Your Benefit | 2026 Max Monthly Benefit |

|---|---|---|

| 62 | Permanently reduced by up to 30% | $2,969 |

| 67 (FRA) | 100% of your earned benefit | $4,207 |

| 70 | 124% of your FRA benefit (8%/year delayed credits) | $5,181 |

Look at that spread: the difference between claiming at 62 and waiting until 70 is $2,212 per month — over $26,500 per year. That’s not a rounding error. That’s a second income.

The average retired worker in 2026 collects just over $2,000 per month. Most people won’t hit the maximums in the table above because those require 35 years of high earnings. But the percentage math is the same for everyone: claim at 62 and lose 30%, or wait until 70 and gain 24% above your FRA amount.

The Break-Even Question Everyone Asks

The most common question people have about delaying Social Security is some version of “how long do I have to live for waiting to pay off?” This is the break-even calculation, and it’s a reasonable place to start — but it’s not the whole picture.

The basic break-even math

If you compare claiming at 62 versus waiting until 67, the person who claimed early collects five extra years of checks. The person who waited gets a larger check every month going forward. The crossover — where total lifetime benefits become equal — is roughly age 78 to 79.

If you compare claiming at 67 versus waiting until 70, the break-even is roughly age 82 to 83.

In plain terms: if you live past your early 80s, delaying almost certainly puts more money in your pocket over your lifetime. Given that a 65-year-old today has roughly a 50% chance of living past 85, the odds favor waiting for most healthy people.

Why break-even analysis alone isn’t enough

Break-even calculations treat Social Security as if it exists in a vacuum. In reality, your claiming decision interacts with at least four other things:

Your tax bracket. Social Security benefits are taxable. Up to 85% of your benefit can be taxed if your combined income exceeds $34,000 (single) or $44,000 (married). A larger benefit from delaying can push more of your income into the 85% taxable tier.

Your Medicare premiums. If your income is above $109,000 (single) or $218,000 (married), you pay IRMAA surcharges on Medicare Part B and Part D. Medicare uses your income from two years prior, so the decision you make about Social Security at 62 or 67 can affect what you pay for Medicare at 64 or 69.

Your spouse’s benefit. When one spouse dies, the survivor keeps the larger of the two Social Security checks — but not both. Delaying the higher earner’s claim to 70 means a bigger survivor benefit for decades.

Your other income sources. If you have a pension, rental income, IRA distributions, or annuity payments, those all affect the tax picture. The years between retirement and age 70 — when you may have low taxable income — can be the best window for Roth IRA conversions that reduce future tax bills and future IRMAA exposure.

When Claiming Early at 62 Actually Makes Sense

Delaying isn’t always the right answer. There are real situations where claiming at 62 is the smart move:

Your health is poor. If you have a serious medical condition or family history that suggests a shorter life expectancy, claiming earlier captures benefits you might not live to collect by waiting.

You need income to avoid high-interest debt. If the alternative to claiming at 62 is running up credit card debt or depleting emergency savings, the guaranteed income may be more valuable than the theoretical benefit of waiting.

You’ve been laid off or can’t find work. The earnings test reduces benefits by $1 for every $2 earned above $24,480 (in 2026) if you’re under FRA. But if you’re not working and have no other income, that doesn’t apply — and Social Security puts food on the table.

You’re the lower-earning spouse in a coordinated strategy. Some couples have the lower earner claim early to provide household income while the higher earner delays to 70, maximizing the eventual survivor benefit.

The Spousal and Survivor Strategy Most People Miss

For married couples, Social Security isn’t just about your own benefit — it’s about protecting the surviving spouse. And this is where the math gets both more important and less intuitive.

How spousal benefits work

A spouse can collect up to 50% of the higher earner’s FRA benefit, even if they have little or no work history of their own. Spousal benefits are available once the higher earner has filed. Importantly, spousal benefits are not increased by delayed retirement credits — they max out at 50% of the worker’s FRA benefit regardless of when either spouse claims.

Why the survivor benefit changes the entire calculation

When one spouse dies, the couple goes from two Social Security checks to one. The survivor keeps the larger check — but the smaller one disappears entirely. If the higher earner delayed to 70 and built up a benefit of $2,480 per month, that becomes the survivor’s check for life. If the higher earner claimed at 62 and locked in $1,400, that’s the survivor’s ceiling.

The difference — $1,080 per month, or nearly $13,000 per year — can be the difference between financial stability and financial stress for a surviving spouse who may live another 15 or 20 years.

The Medicare Connection: IRMAA and the Two-Year Look-Back

This is where Social Security timing connects directly to the retirement planning hub and why this topic sits alongside Medicare underwriting and IUL in the same conversation.

Medicare Part B and Part D premiums are income-tested through IRMAA — the Income-Related Monthly Adjustment Amount. In 2026, the standard Part B premium is $203 per month. But if your modified adjusted gross income from two years ago exceeds $109,000 (single) or $218,000 (married filing jointly), you pay a surcharge that can add hundreds of dollars per month.

How this connects to your Social Security claiming decision

The years between when you retire and when you claim Social Security are often your lowest-income years. If you retire at 63 and delay Social Security until 70, you may have seven years of relatively low taxable income. That window is a gift for two strategies:

Roth IRA conversions. Converting traditional IRA money to a Roth during these low-income years means paying taxes at a lower rate now, and permanently removing that money from future required minimum distributions (RMDs). Roth withdrawals don’t count toward the IRMAA calculation or the Social Security taxation formula.

IRMAA management. Because Medicare uses a two-year look-back, income decisions you make at ages 63 and 64 directly affect what you pay for Medicare at 65 and 66. Keeping income below the IRMAA threshold in those critical years can save $1,000 to $6,500+ per year in Medicare surcharges.

A well-timed Roth conversion strategy — done before Social Security kicks in and before RMDs start — can reduce your tax bill and your Medicare premiums for the rest of your life. But it requires planning, and it requires understanding how Social Security, Medicare, and taxes interact as a system.

Five Questions to Ask Before You File

1. “What is my life expectancy — honestly?” Family history, current health, and lifestyle matter. If longevity runs in your family and you’re in good health, the math strongly favors delaying.

2. “What happens to my spouse if I die first?” The survivor keeps the larger benefit. If you’re the higher earner, your claiming age determines your spouse’s financial floor for the rest of their life.

3. “What does my income look like between retirement and age 70?” If you have pension income, rental income, or can draw from taxable accounts, you may be able to bridge the gap without touching Social Security — and use the low-income years for Roth conversions.

4. “Will my Social Security benefit push me into a higher IRMAA bracket?” Remember the two-year look-back. A large Social Security benefit combined with RMDs from a traditional IRA can trigger surcharges you didn’t expect.

5. “Am I making this decision in isolation or as part of a plan?” Social Security claiming doesn’t exist in a vacuum. The right answer depends on your Medicare coverage, your tax situation, your savings structure, and your spouse’s situation — all at once.

Where Social Security Fits in Your Retirement Plan

Social Security is one piece of a larger puzzle. How you time your claim affects your tax exposure, your healthcare costs, your annuity strategy, and your life insurance structure. That’s why this page exists as part of the Retirement Planning Hub — because none of these decisions should be made in isolation.

I’m not a financial planner or tax advisor. But I see the downstream effects of these decisions every day in my Medicare practice. People who claimed Social Security early without thinking about IRMAA. Couples who didn’t coordinate their claiming strategy and left tens of thousands of dollars in survivor benefits on the table. Retirees who converted too much to a Roth in one year and triggered two years of elevated Medicare premiums.

The best time to think about all of this is before you file — not after.

Have Questions About How Social Security Affects Your Medicare Costs?

I help people understand how Medicare premiums, IRMAA surcharges, and Social Security timing work together. If you’re approaching 65 or already enrolled and want to understand the full picture, let’s talk.

Schedule a Free 30-Minute CallRelated Reading

← Back to the Retirement Planning Hub

Other retirement topics:

The Medicare Supplement Underwriting Trap — Why your health at 65 determines your options for life.

Indexed Universal Life (IUL) Explained — What it is, who it’s actually for, and the red flags to watch for.

Annuities Explained — The five types, real costs, and when they make sense.

What Healthcare Actually Costs in Retirement — The numbers most people don’t plan for. (Coming soon)

Retirement Tax Mistakes — IRMAA triggers, Roth conversions, and income planning. (Coming soon)

Eligry LLC · Cindy Kowalski · Licensed Independent Medicare Advisor · NPN 21601670

(352) 464-4400 · cindy@eligry.com

This content is educational and does not constitute financial, tax, or investment advice. Social Security rules, benefit amounts, IRMAA thresholds, and tax brackets are subject to change. Verify current figures at ssa.gov and Medicare.gov. Consult a qualified financial planner or tax professional before making Social Security claiming decisions. Eligry LLC provides Medicare guidance — not financial planning, tax preparation, or investment advisory services.

We do not offer every plan available in your area. Currently we represent eight carriers which offer 16 products in your area. Please contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program (SHIP) to get information on all of your options. Not affiliated with or endorsed by the U.S. government or the federal Medicare program.

© 2026 Eligry LLC. All Rights Reserved.